Disclaimer: This newsletter is not financial advice it is for educational purposes only. Please DO NOT take this newsletter as a buy or sell signal.

Salesforce Fundamentals:

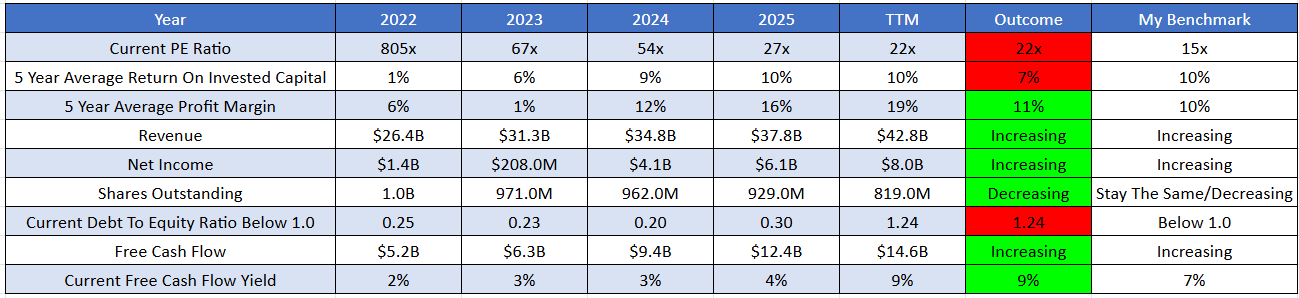

Below is a checklist I normally use when analysing a company’s fundamental health. If the company meets my criteria it will be colour-coded in green and if it fails to meet my criteria it will be colour-coded in red which means I need to investigate further and ask myself why this is the case.

As you can see below there are 3 red boxes and I am going to explain them:

Current PE Ratio - Salesforce currently has a PE ratio of 22x which might indicate that this company is trading at a premium to the market since the average stock market PE ratio is 15x. One thing to remember is that if a company can grow 22% from now until judgment day and can sustain that growth then the current valuation will look cheap. This goes for the opposite side of the spectrum where if a company was trading at 15x earnings and only grew by 3% a year that might seem expensive because the company can’t justify its valuation.

5-Year Average Return On Invested Capital - Return on invested capital (ROIC) reflects how effectively management allocates cash for future growth. When evaluating a company I prefer an ROIC of over 10%. Currently Salesforce has a five-year average ROIC of 7%. This relatively low figure is primarily due to Salesforce's aggressive growth strategy which includes large-scale acquisitions such as Slack, Tableau, and MuleSoft. These acquisitions have significantly inflated Salesforce’s balance sheet with goodwill and intangible assets leading to an exceptionally high invested capital base that has outpaced its net operating profits. Additionally high stock-based compensation and substantial marketing expenditures have further depressed margins. Recently Salesforce’s approach has fundamentally shifted. Salesforce is now prioritising cost-cutting measures, substantial margin expansion, and halting mergers and acquisitions. This conservative approach has caused the company’s operating profits and ROIC to rise rapidly from previous historical lows.

Current Debt-To-Equity Ratio Below 1.0 - Salesforce’s total debt-to-equity ratio has risen to 1.24 because the company launched a historic $50 billion share repurchase authorisation that would be funded by issuing $25 billion in fresh senior corporate notes alongside a new $6 billion term loan used to refinance existing facilities.

Business Overview:

Founded in 1999 by Marc Benioff and Parker Harris, Salesforce is an American software company that specialises in delivering cloud-based enterprise solutions particularly in customer relationship management (CRM) and artificial intelligence. With its headquarters in California, Salesforce operates globally serving clients across the Americas, Europe, Asia-Pacific, and Africa through its innovative cloud platforms and digital applications. The company has established a strong technology ecosystem that offers specialised software for sales, customer service, marketing automation, e-commerce, and data analytics as well as comprehensive developer platforms and business communication tools.

Business Segments:

Agentforce Service - Formerly known as Service Cloud this segment focuses on customer support and helpdesk automation. Agentforce Service delivers omni-channel customer service software that allows enterprises to track, manage, and resolve customer issues smoothly across email, phone, live website chat, and social media. Following its artificial intelligence transformation Salesforce Agentforce Service segment now relies heavily on autonomous AI agents that work 24/7. These digital agents instantly resolve high-volume, repetitive customer inquiries such as processing order returns, checking shipping statuses, or resetting account passwords. By automatically handling these simple tasks and routing highly complex technical cases straight to the right human specialist the software speeds up response times, cuts operational costs for call centres, and directly improves customer retention and satisfaction.

Agentforce Software License - The Sales Cloud segment has historically been anchored by customer relationship management (CRM) software. This software serves as the central digital workspace for sales teams that enables organisations to track new business leads, manage sales pipelines, forecast monthly revenue, and automate client profile data. With the integration of Agentforce AI autonomous sales agents can now operate around the clock to qualify cold prospects, draft highly personalised outreach messages, and automatically manage tedious administrative data entry. By passing these tasks to AI human sales representatives can focus completely on face-to-face client relationships to close larger deals.

Agentforce 360 Platform, Slack and Other - This segment represents the underlying digital infrastructure, customisation layer, and collaborative heart of Salesforce. Salesforce Agentforce 360 platform provides developer tools, low-code drag-and-drop builders, and app-building frameworks that allow companies to build completely tailored business applications on top of the standard Salesforce architecture. This segment also houses Slack which serves as the central collaborative workspace and primary conversational interface for an organisation.

Agentforce Integration and Analytics - This data-centric segment combines two massive software platforms MuleSoft and Tableau. Salesforce Agentforce Integration and Analytics segment focuses on connecting separate, messy enterprise data silos, legacy software applications, and external APIs across an organisation using MuleSoft’s powerful integration engine. Once that data is securely connected and flowing Tableau provides advanced data visualisation tools, interactive dashboards, and business intelligence reports. Together these two systems act as the enterprise’s nervous system by transforming disorganised raw data into clear visual insights for executives while simultaneously supplying the clean, unified, real-time data foundation that autonomous AI agents strictly require to make precise, safe, and accurate business decisions.

Agentforce Marketing and Commerce - This segment merges Salesforce’s digital experience tools to optimise how businesses attract customers and secure online sales. Agentforce Marketing automates multi-channel marketing campaigns across email, SMS, and mobile apps using real-time customer behaviour to instantly customise promotional messages and generate digital content.

Professional Services and Other - Unlike the rest of Salesforce’s subscription-based software segments this category consists of human-driven consulting, implementation services, and technical training. Salesforce Professional Services also captures the revenue generated by Salesforce’s internal consulting experts, project managers, and certified software architects who partner directly with large global enterprise clients to design, deploy, and safely configure highly complex, large-scale software systems. While their consulting business generates much lower profit margins than selling pure software licenses this segment is important for the company’s long-term success because it ensures that giant corporate clients properly set up their databases, successfully adopt new AI tools, and scale their technology ecosystems without costly operational downtime.

Management:

When evaluating management I judge the CEO based on several factors such as experience, capital allocation skills, and Incentives. In this section I will discuss whether management incentives are aligned with shareholders’ interests.

Experience - Marc Benioff co-founded Salesforce in March 1999 and has served as the company’s Chief Executive Officer for over two decades. His academic foundation began at the University of Southern California (USC) where he graduated in 1986 with a Bachelor of Science in Business Administration. Decades later his ongoing contributions and connection to the institution led USC to award him an Honorary Doctor of Humane Letters degree alongside a seat on its Board of Trustees.

Marc Benioff has a lot of experience in the software world. His entrepreneurial instincts showed early when he founded Liberty Software at age 15. During his college years he secured an internship at Apple where he wrote assembly code for the Macintosh division. Upon graduating from USC Marc Benioff joined Oracle Corporation where he spent 13 years in sales, marketing, and product development. He rose rapidly through the ranks and was named Oracle’s Rookie of the Year at age 23 and eventually became the youngest Vice President in the company’s history at just 26. Marc Benioff maintained this high-level executive position until 1999 when he chose to leave his established corporate career to pioneer the cloud computing industry by launching Salesforce from a rented apartment in San Francisco.

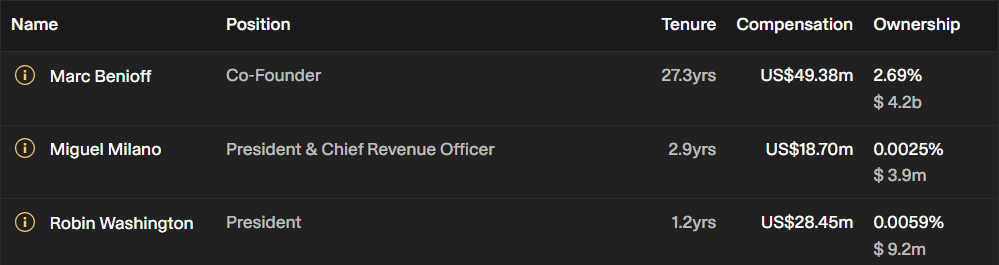

Below is an image illustrating the current experience of Salesforce board members:

Capital Allocation - Capital allocation is very important when judging management because I want them to create value for shareholders not destroy it. Salesforce has changed its capital allocation strategy from a growth-at-all-costs philosophy to an aggressive focus on operating efficiency and massive capital returns.

Marc Benioff’s capital allocation strategy was historically characterised by heavy equity dilution to fund high-profile acquisitions like Slack, Tableau, and MuleSoft. While these deals expanded Salesforce’s tech ecosystem they also inflated the equity base and depressed the company’s Return on Invested Capital (ROIC). Under pressure from activist investors Marc Benioff completely overhauled this approach. Today he primarily allocates capital to reducing the company’s share count, cutting costs, and driving organic margin expansion through the new Agentforce AI framework rather than pursuing highly dilutive multibillion-dollar corporate takeovers.

Salesforce's board authorised a $50 billion share buyback program. Marc Benioff launched a $25 billion accelerated share repurchase (ASR) program to aggressively buy back over 100 million shares at what management views as an undervalued stock price. This aggressive buyback framework is designed to reverse years of shareholder dilution, offset stock-based compensation, and systematically boost earnings per share (EPS). In addition to the massive buybacks Benioff has committed to a highly reliable and recurring quarterly dividend policy.

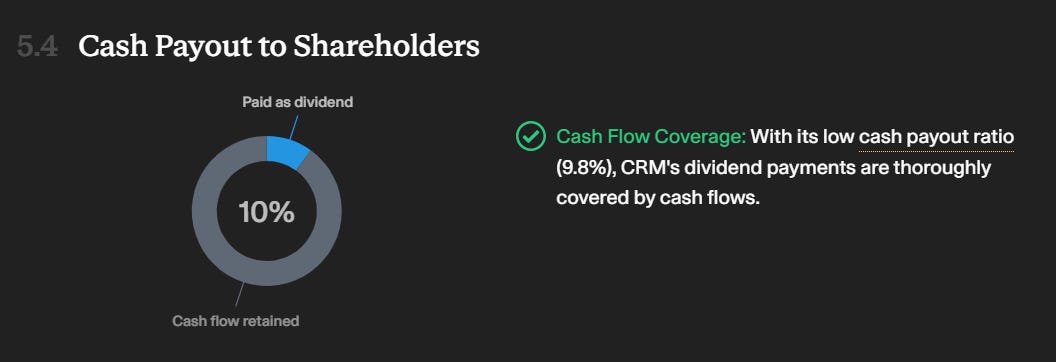

Salesforce currently offers a dividend yield of approximately 0.92%. This dividend is sustainable because it only covers 10% of the company’s free cash flow.

Incentive- This is important because if the current board is buying shares of their own business it indicates that management believes the stock is undervalued and is confident in the company’s long-term prospects.

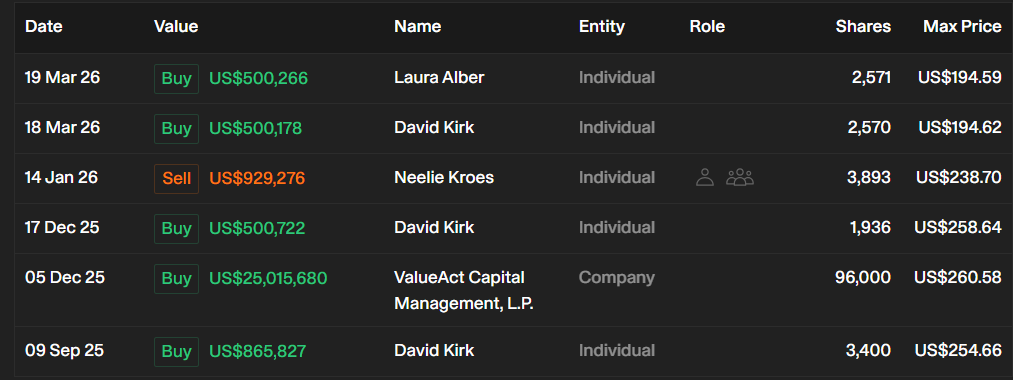

As you can see below we have 5 buy and 1 sell order. Laura Alber, David Kirk and ValueAct Capital Management are the only insiders buying Salesforce shares. As for selling Neelie Kroes is the only insider selling but I won’t put weight on this because there are so many reasons why someone might sell their stock.

Bull And Bear Case:

Bull Case

Bull Case - The first bull case is Salesforce Rapid Scale of Agentforce AI. Salesforce's shift into agentic AI is monetising far faster than Wall Street anticipated. Salesforce Agentforce’s annual recurring revenue (ARR) has surpassed $1.2 billion demonstrating that enterprise clients are actively adopting autonomous digital agents.

Bull Case- The second bull case is Margin Expansion. Following aggressive cost-cutting and a structural exit from their growth-at-all-costs era Salesforce has successfully pushed its non-GAAP operating margins to an industry-leading 34.8%.

Bull Case- The third bull case is Aggressive Shareholder Yields. Management has aggressively prioritised capital returns. The company returned a massive $27.1 billion via share repurchases in a single quarter backed by a board-authorised $50 billion buyback framework that eliminates historical equity dilution.

Bear Case

Bear Case- The first bear case is Core Markets Maturity. Slower growth patterns suggest that Salesforce’s foundational markets specifically CRM (Sales) and customer service software are rapidly approaching domestic saturation. This makes double-digit organic seat expansion much harder to maintain.

Bear Case- The second bear case is the risk of Seat-Count Contraction. The core business model relies heavily on charging software licensing fees per human seat. If the company’s own autonomous AI agents become highly efficient enterprise clients may dramatically reduce their human headcount. This will create a long-term structural downward pressure on seat-based revenues.

Bear Case- The third bear case is AI Competition. Salesforce faces direct competition in the enterprise AI space from tech giants. Competitors like Microsoft (with Copilot) and ServiceNow are aggressively racing to build alternative layers for business orchestration and automation.

Valuation:

In this section I will discuss valuation. Using some basic metrics I will compare Salesforce to its industry rival and determine whether the company is cheap relative to its peers. Then I will value Salesforce using a discounted cash flow model to determine a price I am willing to pay based on its expected growth rate and my desired return of 15%.

As shown below when compared to its peers Salesforce scores 4/5 while Microsoft scores 1/5. Below I am going to highlight the key differences between the companies:

Business Model - Salesforce operates a specialised cloud software model that focuses entirely on helping businesses manage, organise, and automate their customer relationships. Salesforce is currently shifting away from traditional per-user subscription fees to charge directly for autonomous AI agents that perform administrative and sales tasks.

Microsoft on the other hand operates a highly diversified technology platform model that relies heavily on bundling everyday workplace software alongside its own global cloud computing network(Azure). While Salesforce focuses all its energy on locking enterprises into its high-margin customer data systems Microsoft uses its immense scale to sell giant packages of computing infrastructure, security, and office utilities which allows them to undercut competitors.

Market Reach - Salesforce focuses its market presence on customer-facing departments within businesses where it has a strong influence over global sales teams, customer service desks, and marketing divisions. Salesforce primarily concentrates on the applications that employees use to communicate with clients outside the company.

Microsoft has a broader reach because its technology powers the operating systems on workers’ desktops and the backend servers that keep global companies operating daily. In recent years Microsoft has taken advantage of its established position to enter Salesforce’s territory. They have started selling their own competing business software to the large number of corporate clients that already use Microsoft infrastructure.

Product Offering - Salesforce is the leader in customer management software. They offer a connected set of applications called Customer 360 along with data tools such as MuleSoft and Tableau. This software allows companies to track every customer interaction and turn messy business data into clear visual charts for managers.

Microsoft’s product range is much broader and serves as a daily utility for businesses worldwide. Microsoft’s product range includes the Windows operating system, Xbox gaming, and the Microsoft 365 office suite which includes Teams, Word, and Excel. While Salesforce focuses on creating smart AI agents that automate data entry and customer service tasks Microsoft integrates its AI assistants directly into regular office programs to help employees manage their daily emails, spreadsheets, and meetings.

As you can see based on my conservative assumption Salesforce is looking to grow 9% over the long run so I went conservative and assumed a 7% growth in the first 1-3 years then the growth will slow down to 4% 4-6 years out. In my assumption I also went with an exit multiple of 15x earnings which is below the historical average at which Salesforce has traded. Based on my assumption I have come to a buy price of $219.00 compared to the current stock price of $191.10 which means right now Salesforce is trading below its intrinsic value.

Thanks for reading my newsletter on Salesforce.

Disclaimer: This newsletter is not financial advice. This is for educational purposes only, so please DO NOT take this as a buy or sell signal.

Follow for more:

Remember to subscribe, share, and comment below if you find this newsletter insightful. Your support helps me continue my work.