InvestingWithWes Annual Letter-2022

InvestingWithWes Annual Letter-2022

Is It Different This Time?

Disclaimer this newsletter is not financial advice this is for educational purposes only so please DON’T take this as a buy or sell signal.

Dear Followers,

Welcome to the first edition of my annual letter. In this letter, I will be reflecting on my investing journey in 2022 and I hope everyone reading this can gain some sort of value from it. I will be talking about my mistakes, the current market condition, content creation and how I will be investing going forward into the new year and beyond.

Content Creation

2022 has been great for me in terms of content creation on Instagram. My Instagram page is currently at 3.7K followers and I can’t thank every one of you enough for following and supporting me throughout 2022. The exponential growth of my Instagram has given me many opportunities for myself as I was able to meet new people from all walks of life as well as being able to have the opportunity to show up as a guest on various podcasts like The Take Off Experience Podcast and Make It Stack Podcast. I thank both hosts for allowing me to come on their platform to share my investing perspective. In late 2022 I also launched my Substack, free for anyone to view. Since the launch of my free Substack in September I have gained 100 new followers so I thank every one of you for supporting my monthly write-up. My Substack is geared towards a niche of followers as it is mainly based on independent research on special situations and small-cap companies. The reason why it is geared around this niche is that as a retail investor who hasn’t got billions of dollars to move around like the super investors we follow I have acknowledged that I have an advantage over these people because they can’t buy into smaller and obscure companies for different reasons such as, investing in something small isn’t enough to move the needle financially so institutions and fund managers are forced to look in the upper end of the market cap spectrum. If I can spend most of my investing career focusing on this niche I should be able to generate outsize returns.

Investing Mistakes

2022 was my real first year as a value investor and I must say I am proud of the way my first year has gone because a majority of that year was spent trying to find my identity as an investor. Even though I am happy with my first year, I still want to reflect on things that I could have done differently as I feel I made two errors in the early stages of my value investing career. The first mistake I made is overpaying for two companies by not being conservative enough. The first company is Meta Platforms. Meta is currently my third largest holding in my portfolio and I firmly believe the current situation that investors are pricing in on this company is very much exaggerated but I feel I could have bought the company at a much better margin of safety. My average price for Meta is currently $188 but I originally started buying Meta at $314 a share which was a mistake because I over projected that the company will continue to grow 15% a year which was silly of me in the first place. Even though I made that mistake I have now learnt to be more conservative so that mistake doesn’t happen again. Even though I made this mistake I still live on to fight another day because of my margin of safety. Due to me having a much higher original buy price than I wanted, my return on Meta has gone from a potential 15% return to a 7% return. I will take that as long as it’s not a permanent loss of capital. This is why I stress the importance of investing with a large margin of safety because we are humans and we do make mistakes and when the mistake happens you can still live on to fight another day.

The second mistake I would like to focus on is PayPal. This was another company I overpaid for early on in my value investing career by not being conservative enough. When I was valuing PayPal I was projecting that the company would continue to grow 15% in revenue but since then their projection keeps decreasing to the point where the company is now looking to grow at a rate of 7-10% going forward. Even though I over-projected the rosiest of assumptions on PayPal I continue to live on to fight another day due to my margin of safety where my returns have gone from 15% to 7% which is still good, especially in today’s market. On 19th August, I ended up selling PayPal for a 30% return because the stock went up so quickly.

Error Of Omission

Warren Buffett often talks about making errors of omission. Errors of omission is a mistake that consists of not doing something that you should have done. This year this happened to me on three different occasions and it has cost me a lot of money and potential returns. The three occasions it happened were with 1-800-Flowers, Supreme PLC and Crocs. Each of these stocks has gone up by 40-50% from when I was looking at them but I could not push the buy button because one I didn’t have the cash and two I always felt like I was missing something despite knowing everything about these companies. In a moment like this, it is important to have cash on the side-line and trust your judgment and not overcomplicate things.

Is It Different This Time?

“History doesn’t repeat itself but it does rhyme”-Mark Twain. Throughout history, we have seen bubbles come and go and the nifty-fifty growth stock bubble was one example where investors thought the best companies in America were unbeatable. This list of companies that got caught up in the bubble was:

American Express

American Home Products

American Hospital Supply Corporation

AMP Inc.

Anheuser-Busch

Avon Products

Baxter International

Black & Decker

Bristol-Myers

Burroughs Corporation

Chesebrough-Ponds

The Coca-Cola Company

Digital Equipment Corporation

Dow Chemical

Eastman Kodak

Eli Lilly and Company

Emery Air Freight

First National City Bank

General Electric

Gillette

Halliburton

Heublein

IBM

International Flavours and Fragrances

International Telephone and Telegraph

JCPenney

Johnson & Johnson

Louisiana Land & Exploration

Lubrizol

Minnesota Mining and Manufacturing (3M)

McDonald's

Merck & Co.

MGIC Investment Corporation

PepsiCo

Pfizer

Philip Morris Cos.

Polaroid

Procter & Gamble

Revlon

Schering Plough

Joseph Schlitz Brewing Company

Schlumberger

Sears, Roebuck and Company

Simplicity Pattern

Squibb

S.S. Kresge

Texas Instruments

Upjohn

The Walt Disney Company

Walmart

The peak PE Ratio of the Nifty Fifty stocks was 60-90x earnings but once the bubble popped these companies traded down to a PE ratio of 6-9x earnings. In this bubble, investors lost 90% of their money and this was a lesson in why valuation matters in the long run.

The Dot Com bubble occurred when there was a rapid rise in stock price and valuation by internet companies that simply had Dot Com in their name. This happened all because the speculation was that the internet was going to be the next big thing which it was but very few companies during that era survived because most of the companies back then had little to no revenue and earnings. This was another lesson for investors as a lot of money was lost and most of the Dot Com stock didn’t return to its former highs until 10 years later or never fully recovered at all. Below are 3 links of me giving such examples.

What Does Overpaying For Growth Look Like? Part 1

What Does Overpaying For Growth Look Like? Part 2

What Does Overpaying For Growth Look Like? Part 3

In the last 2/3 years, we have seen speculation once again in many different asset classes such as cryptocurrency, the stock market and NFTs as many new investors have entered the market. For those who aren’t familiar cryptocurrency is a digital currency in which transactions are verified and records maintained by a decentralised system using cryptography, rather than by a centralised authority. I for one have never speculated in cryptocurrency because I don’t know how to put a value on something that doesn’t produce cash flow so I avoid it like many things. In November 2021 Bitcoin peaked at $69,000 before falling to the current price of $16,646.

We have seen speculation in NFT in the last few years where a picture of rock sold for $1.7 million but what is an NFT? An NFT or non-fungible token is a unique digital identifier that cannot be copied, substituted, or subdivided, recorded in a blockchain, and used to certify authenticity and ownership. The ownership of an NFT is recorded in the blockchain and can be transferred by the owner, allowing NFTs to be sold and traded. NFTs can be created by anybody, requiring few or no coding skills. NFT’s typically contain references to digital files such as photos, videos, and audio. Because NFTs are uniquely identifiable assets, they differ from cryptocurrencies, which are fungible. I for one have never touched an NFT because I can’t put a value on it.

In recent years the stock market has been compared to a casino as we have seen wild speculation in many different parts of the market such as non-profitable tech companies, Ark innovation fund, EV companies and the rise of SPACS. In 2022 the stock market is down 19.70% YTD with Ark being the poster boy of this bubble currently down 68.52% YTD. Ark is an actively managed Exchange Traded Fund(ETF) that seeks long-term growth of capital by investing under normal circumstances primarily (at least 65% of its assets) in domestic and foreign equity securities of companies that are relevant to the Fund's investment theme of disruptive innovation. ARK defines ‘‘disruptive innovation’’ as the introduction of a technologically enabled new product or service that potentially changes the way the world works. Below is an image of the top 18 holdings of this ETF.

How To Recognise And Avoid The Next Bubble?

SPACS-You might not be familiar with SPACs but SPACs stand for special purpose and acquisition. SPAC is a shell company when it goes public which means it has no existing operations or assets other than cash and any investments. Warren Buffett and Charlie Munger have spoken strongly against SPACS as it is seen as a cheap way for terrible companies to go public and we have seen that within the last few years where companies like Clover, DraftKings, and Tattoo Chef have all gone public via the SPAC route. In 2021 alone 613 companies went public Via the SPAC route because it was easy to raise money and sell your product to banks and retail investors as retail investors who just entered the market were hungry to just put their money to work regardless of the quality of the asset.

Bull Market Celebrity-“The investment business is full of people who get famous for being right once in a row”-Howard Marks. In every extended bull market, there is always that one celebrity that is shown on your television screen constantly because they got lucky on one prediction. In this bull market that celebrity was Cathie Wood. Cathie Wood owns the Ark Innovation fund and the main theme of that fund was to invest in the technology of the future. March 2020 was when Cathie Wood started to make a name for herself as her fund started to soar quickly in value and by October 2020 her fund went to $90 a share from $37 which was the low of the market crash. Cathie Wood got her fame from investing in companies like Palantir(sold), Block and Teladoc but one particular trade that made her ETF go up quickly in value was Tesla. In the last 2 years, Tesla has been her clear outstanding winner but as we headed into 2022 things came crashing down as the market started to go against Cathie Wood. Despite predicting one winner in her portfolio her ETF is down 68.52% YTD which shows following the trend is a loser's game once the tide goes out.

New FADs-In every bull market, there is always a new FAD whether that is the way we invest or something as simple as using different metrics to justify buying overpriced securities. Within the last few years, you were told if you didn't buy these new and disruptive companies that were going IPO you were out of touch and not with the new age of investing. Even Warren Buffett who has been investing since he was a kid got told his value investing philosophy was outdated by the new breed of investors with barely any track record. As the bull market started to progress new investors were using the price-to-sales ratio as a way to justify paying ridiculous valuation for stocks when in reality real earnings and cashflow are what truly matters. Any company can sell a product if they make it exciting enough but making real cash flow and earnings is difficult and a lot of companies that went public during the last 2/3 years didn’t have either.

Unprofitable Tech IPO’s-During the last few years, we saw a record amount of companies taking advantage of fresh money entering the market. Companies such as Uber, Peloton, and Palantir all went public via the traditional IPO route but had little to no earnings to justify a high valuation.

New Stock Market Participants-Most participants treat the stock market like a gambling parlour where everyone wants to get rich quickly with that one lottery ticket stock and that has proven to never work over the long run. Investing is about staying in the game to allow your money to compound and the way to do this is to concentrate on hitting the singles and the occasional doubles and not go looking for home runs. If you have a portfolio with expensive stocks hoping they can be the next big thing you will get wiped out compared to someone who has a portfolio with the risk under control by protecting his downside with a margin of safety. I compare this to baseball where if you keep it simple and get to base each time you will do well compared to someone more focused on getting home runs and looking for the spectacular which is difficult as you have a higher chance of getting out than actually getting the home run itself.

Herd Mentality-In the famous words of Seth Klarman "The herd is always wrong". During the last few years, we have seen a prime example of herd mentality in action where new market participants have driven the stock price of companies way above their fundamentals. A great example of herd mentality in action is investors driving PayPal from $86 a share to as high as $308 which is a gain of 256% in less than 12 months. If you studied stock market history you would know that this amount of gain within a short amount of time is not sustainable and yet again it wasn't different this time as PayPal fell 76% from its peak of $308 a share. PayPal is just one example because there is Palantir, Shopify, Teladoc and countless others who fell victim to herd mentality as investors were in rush to sell due to expectations being too high. As Benjamin Graham stated the stock market in the short run is a voting machine so what is popular will win but in the long run, it is a weighing machine so what is behind the company will ultimately decide a company destination and if you can’t produce cashflow and earnings when it matters the most then the stock is in trouble.

The Average Joe-This reminds me of the Peter Lynch cocktail party theory where if you go to a cocktail party and someone asked you what stocks are you buying and if you tell them your picks and they seem not interested then chances are stocks are cheap but if you go to a cocktail party and everyone is lecturing you to invest in a company because it promises great returns due to its great growth potential then chances are stock might be expensive. This reminds me of the time when I was having a conversation with a friend at work and a colleague asked me about Bitcoin while interrupting my conversation. At that moment I was shocked because I have worked at this place for years now and never have I ever heard her talk about investing. We normally get this sort of behaviour when an asset is at the peak of its popularity.

How To Avoid The Next Bubble-There are many ways to avoid the next bubble and FAD. My tip for avoiding the next bubble is to study stock market history because you will notice how similar events are but the characters are different. Another tip I give to investors is to read books because I find it easy to learn from the experience of other investors such as Warren Buffett, Howard Marks etc. It is better to learn from other people’s experiences than to experience the pain yourself.

My 2022 Performance

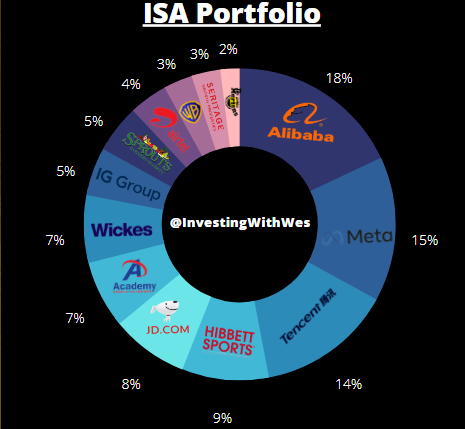

I have been value investing for about 1.6 years now and I am pleased with my performance considering the market condition we are in. In terms of my investment portfolio, I own the following companies:

Alibaba-BABA

Meta Platforms-META

Tencent-TCEHY

Hibbett Sports-HIBB

JD-JD

Academy Sports And Outdoors-ASO

Wickes PLC-WIX.L

IG Group-IGG.L

Sprouts Farmers Market-SFM

Airtel Africa-AAF.L

Warner Bros Discovery-WBD

Seritage Growth Properties-SRG

Dr Martens-DOC.L

Stats

💵 YTD: -4.68%

📶 CAGR: -4.51% (1.6 years)

📊 SPY CAGR Returns: -14.25%

📈 All-Time Best Performers:

$SFM +68% | $ASO +64%

📉 All-Time Worst Performers:

$META -34% | $WBD -35%

Strategy going into 2023-My strategy will remain the same as always and nothing will change. I will continue to buy securities where I see there is some sort of mispricing. I will continue to focus on special situations and small caps as I believe these sorts of areas will provide me with the best chance of outsize returns as a small investor.

Thanks for reading my newsletter. Disclaimer this newsletter is not financial advice this is for educational purposes only so please DON’T take this as a buy or sell signal.

Follow for more:

Don’t forget to subscribe, share and leave a comment below if you found this newsletter insightful as it helps support my work.

Thanks for this, really good perspective! Curious why you own both Hibbett and ASO, where do you see the case right now.

Excellent letter. Very detailed with track record of what happened in the market this year. Looking forward to 2023 letter already! Happy New Year!