Disclaimer: This newsletter is not financial advice it is for educational purposes only. Please DO NOT take this newsletter as a buy or sell signal.

Intuit Fundamentals:

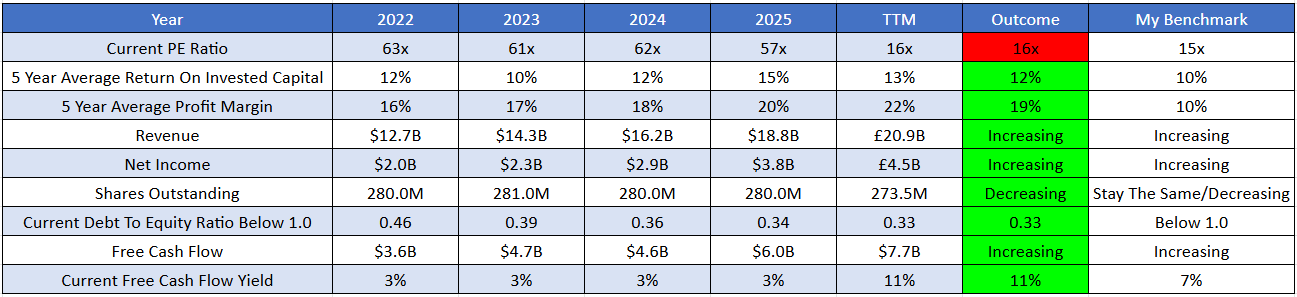

Below is a checklist I normally use when analysing a company’s fundamental health. If the company meets my criteria it will be colour-coded in green and if it fails to meet my criteria it will be colour-coded in red which means I need to investigate further and ask myself why this is the case.

As you can see below there is 1 red box and I am going to explain it:

Current PE Ratio - Intuit currently has a PE ratio of 16x which might indicate that this company is trading at a premium to the market since the average stock market PE ratio is 15x. One thing to remember is that if a company can grow 16% from now until judgment day and can sustain that growth then the current valuation will look cheap. This goes for the opposite side of the spectrum where if a company was trading at 15x earnings and only grew by 3% a year that might seem expensive because the company can’t justify its valuation.

Business Overview:

Founded in 1983 by Scott Cook and Tom Proulx, Intuit is an American financial technology platform whose primary business involves the development and sale of financial, accounting, and tax preparation software and related services. Headquartered in California, Intuit operates globally serving consumers, small businesses, and accounting professionals across North America, Europe, Australia, and other international markets primarily through its cloud-based software-as-a-service (SaaS) ecosystems. The company’s product offerings include QuickBooks for small business accounting and payroll, TurboTax for consumer tax filing, Credit Karma for personal finance and credit monitoring, and Mailchimp for email marketing and business automation. Intuit also provides specialised software suites and professional services tailored directly to certified accountants and tax practitioners.

Business Segments:

Global Business Solutions - The Global Business Solutions segment has become Intuit’s largest division accounting for 59% of the company’s total revenue. This segment primarily serves small to medium-sized businesses as well as accounting professionals with a strong focus on their QuickBooks ecosystem. Its product offerings include cloud-based accounting software, payroll processing, merchant payment solutions, and business management tools. Additionally it includes Mailchimp for marketing automation.

Consumer - The Consumer segment is Intuit’s second-largest segment accounting for 26% of the company’s total revenue. This segment is centred around the TurboTax ecosystem which provides do-it-yourself and assisted digital tax preparation services for individuals. Demand for this product is typically seasonal with the majority of sales and customer acquisitions occurring during the peak tax-filing season from January to April.

Credit Karma - The Credit Karma segment which accounts for 12% of Intuit’s total revenue serves as the company’s personal finance platform. It provides users with free access to credit scores, credit monitoring, and various financial health tools. Revenue for this segment is generated through a business-to-business model where financial institutions pay Intuit for targeted data-driven consumer matchmaking services related to credit cards, personal loans, auto insurance, and home financing.

ProTax - ProTax is Intuit’s smallest segment accounting for 3% of total revenue. This segment serves a highly specialised and strategic purpose within the professional ecosystem by offering cloud-based and desktop tax-preparation software suites including ProConnect Tax, Lacerte, and ProSeries. These products are specifically designed for certified public accountants (CPAs), enrolled agents, and professional tax firms.

Management:

When evaluating management I like to judge the CEO based on several factors such as experience, capital-allocation skills, and Incentives. In this section I will discuss whether management incentives are aligned with shareholders.

Experience - Sasan Goodarzi took over as Intuit’s Chief Executive Officer in January 2019 and has served as the company’s leader for several years. His academic foundation began at the University of Central Florida where he graduated with a Bachelor of Science in Electrical Engineering. Years later his ongoing commitment to business leadership led him to earn a Master of Business Administration from the Kellogg School of Management at Northwestern University.

Sasan Goodarzi has a lot of experience in the technology field. He co-founded Lazer Cables INC and served as its CEO. In his early career he worked at Honeywell for 9 years and rose to become Vice President and Managing Director for Mid America. After his time at Honeywell he gained more executive skills as the Global President of the Products Group at Invensys. In 2004 he joined Intuit where he spent 15 years moving quickly through the ranks and eventually became the CEO.

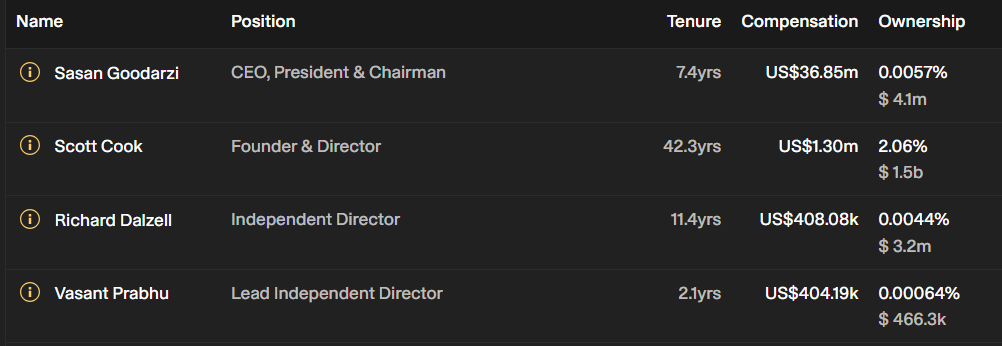

Below is an image illustrating the current experience of Intuit board members:

Capital Allocation - Capital allocation is very important when judging management because I want them to create value for shareholders not destroy it. Intuit has consistently followed a disciplined capital allocation strategy that combines strategic acquisitions aimed at expanding its platform with steady and aggressive returns of capital to its shareholders.

Sasan Goodarzi’s approach to capital allocation has primarily focused on mergers and acquisitions to expand Intuit’s addressable market. Examples of this strategy include the $7.1 billion acquisition of Credit Karma and the $12 billion purchase of Mailchimp. While these deals have successfully integrated new consumer and marketing ecosystems into Intuit they also require substantial capital investment and shift the company’s focus toward post-acquisition integration. In addition to these acquisitions Sasan Goodarzi is prioritising shareholder value by approving a new $8 billion share repurchase program. To further align with investor interests and demonstrate confidence in the company’s future Sasan Goodarzi and his executive leadership team have completely cancelled their pre-scheduled stock sale plans.

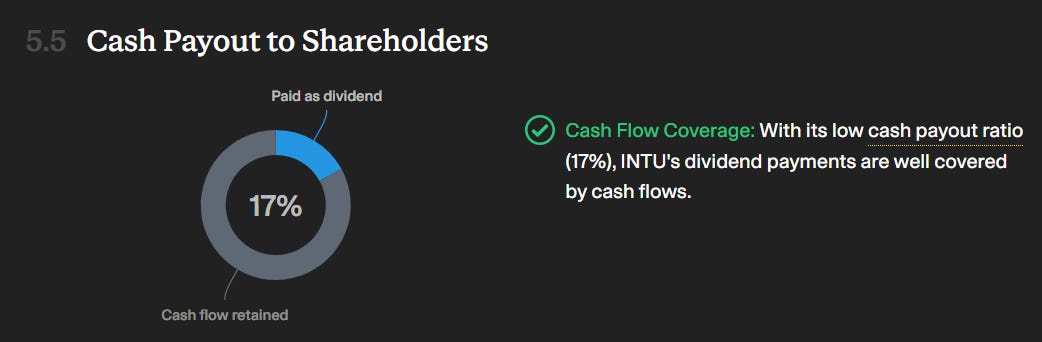

Intuit currently pays a dividend with a yield of 1.80%. This dividend is sustainable because it only covers 17% of the company’s free cash flow.

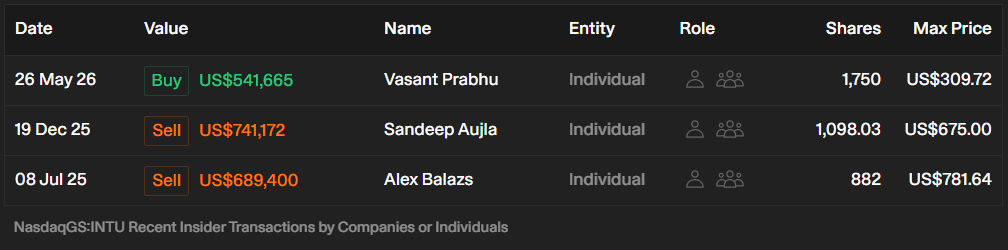

Incentive - This is important because if the current board is buying shares of their own business it indicates that management believes the stock is undervalued and is confident in the company’s long-term prospects.

As you can see below we have 1 buy and 2 sell orders. Vasant Prabhu(Lead Independent Director) is the only insider buying Intuit shares. As for selling Sandeep Aujula(Vice President/Chief Finance Officer) and Alex Balazs(Executive Vice President/CTO) are the only insiders selling but I won’t put weight on this because there are so many reasons why someone might sell their stock.

Bull And Bear Case:

Bull Case

Bull Case - The first bull case is Intuit High Switching Costs & Monopoly. The core ecosystems of QuickBooks and TurboTax have a strong economic advantage. When a small business integrates its payroll, invoicing, inventory, and tax compliance into QuickBooks the challenges and risks associated with switching to a competitor become significant. This can lead to highly loyal customer groups and highly predictable recurring revenue from their software-as-a-service (SaaS) model.

Bull Case - The second bull case is The Monetisation of Generative AI via Intuit Assist. Rather than being disrupted by AI Intuit is using its financial data to fuel its generative AI layer. By acting as an automated financial control tower the platform automates complex workflows and enhances decision-making that drives higher average revenue per user (ARPU) as clients willingly pay a premium for software that proactively saves them time and money.

Bull Case - The third bull case is Shareholder-Friendly Capital Returns. Intuit operates an incredibly cash-generative business model with a high Return on Invested Capital (ROIC). Management uses this free cash flow to reward long-term shareholders with the company recently approving a new $8 billion share buyback authorisation alongside a 15% increase in its quarterly dividend which drives shareholder value.

Bear Case

Bear Case - The first bear case is The Breakdown Of The Per-Seat SaaS Model (Agentic AI Disruption). The biggest structural threat to Intuit’s long-term valuation is the rise of autonomous AI agents. Investors fear that next-generation generative AI tools from companies like OpenAI, Anthropic, or specialised platforms like Perplexity Tax will automate entire financial workflows (bookkeeping, invoicing).

Bear Case - The second bear case is Near-Stagnant Volume Growth in TurboTax Online. As a direct consequence of these pricing missteps and a maturing domestic market Intuit announced that TurboTax online paying units are expected to grow by only 2%. Relying almost entirely on aggressive price hikes rather than on customer acquisition to drive revenue growth is an unsustainable long-term strategy.

Bear Case - The third bear case is Failure and Pricing Missteps in the DIY Tax Market. In the company’s fiscal Q3 2026 results they revealed severe cracks in its core TurboTax segment where Management openly admitted they had lost on price meaning the company failed to successfully capture or retain the most price-sensitive do-it-yourself (DIY) tax filers. The pricing mismatch forced a major downward re-evaluation of its market positioning.

Valuation:

In this section I will discuss valuation. Using some basic metrics I will compare Intuit to its industry rivals and determine whether the company is cheap relative to its peers. Then I will value Intuit using a discounted cash flow model to determine a price I am willing to pay based on its expected growth rate and my desired return of 15%.

As shown below when compared to its peers Intuit scores 2/5, The Sage Group PLC scores 2/5 and Xero Limited scores 1/5. below I am going to highlight the key differences between each company:

Business Model - Intuit operates a complete financial technology ecosystem powered by AI. Their strategy focuses on customer retention by managing both the accounting ledger and related financial services. Intuit generates revenue through a multi-product model in which it charges subscriptions based on the number of users or service tiers. Additionally they earn high-margin transaction revenue from services such as payroll processing, merchant services, and integrated consumer credit matching. To expand their business Intuit relies heavily on aggressive multibillion-dollar acquisitions. They purchase entire customer ecosystems such as Mailchimp and Credit Karma and integrate them into their centralised data-driven AI cloud.

The Sage Group utilises a tiered hybrid deployment model designed for enterprise-level scalability, compliance, and strong corporate trust. Unlike Intuit which focuses on micro-businesses Sage addresses a broader range of needs from basic cloud bookkeeping to complex on-premises and cloud-native Enterprise Resource Planning (ERP) systems like Sage Intacct. One of Sage’s key advantages is its strong localised compliance engine and the ability to customise solutions for specific industries. This setup allows the company to effectively support mid-market and enterprise operations by offering detailed role-based permissions, advanced inventory management, and complex multi-entity consolidation.

Xero Limited operates on a cloud-native, open-ecosystem Software-as-a-Service (SaaS) model that prioritises simplicity, a modern user experience, and enhanced collaboration with accountants. Unlike Intuit which tries to create or buy every financial service Xero sees itself as a central hub that allows businesses and their financial advisors to share information easily through a single system. Xero’s key advantage is its open API integration marketplace which includes over 1,000 third-party applications. The platform also features a competitive pricing model that allows unlimited users on its standard tiers for each organisation. Lastly Xero’s growth strategy is agile and network-driven and relies heavily on recommendations from accounting practices to organically promote the platform to small businesses.

Market Reach - Intuit’s market reach is heavily concentrated in North America where it holds a monopoly-like grip on the US consumer tax and small business accounting software sectors. While it operates a global footprint its international expansion outside of North America is targeted and secondary. Intuit relies on massive marketing spend and brand presence to lock down its core markets and aggressively defend its borders against international newcomers.

The Sage Group is an established multinational with a deep global footprint particularly across the United Kingdom, continental Europe, North America, and Africa. They have a strong local presence because they customise their services to meet the specific tax and payroll rules of each country. Instead of trying to quickly gain a lot of users Sage focuses on building deep relationships with mid-sized businesses and established companies in Europe.

Xero Limited is a rapidly growing global player born in New Zealand. It maintains a dominant presence over the Australasian (Australia and New Zealand) cloud accounting markets. Over the last decade Xero has aggressively expanded its presence in Europe, emerging as a leading cloud-first force in the United Kingdom and actively pushing its cloud ecosystem into South Africa, Southeast Asia, and the highly competitive North American market to directly challenge Intuit.

Product Offering - Intuit is a leader in do-it-yourself tax preparation, automated bookkeeping, and credit lead generation. It offers a wide range of financial tools that work well together. Its main products include QuickBooks, TurboTax, Credit Karma, and Mailchimp which are made to help users manage their business and personal finances easily. With these tools you can automate tasks like filing taxes, sending invoices, marketing, and tracking cash flow all with one login.

The Sage Group’s product offering is more traditional, precise, and engineered for heavy-duty financial management. Their main areas are core accounting, market-leading enterprise payroll, and ERP software configurations including Sage 50, Sage 200, and Sage Intacct. This software manages multi-currency workflows, granular auditing, and complex supply chain logistics. While they also offer basic invoicing for small businesses their strength lies in providing financial reporting for companies that need more than basic tools.

Xero Limited products are focused on the day-to-day operational workflow of small to medium-sized businesses. Their platform focuses on user-friendly invoicing, automated receipt capture, and bank feed reconciliation. While Xero provides basic inventory management and cash flow reporting capabilities it leverages a wide range of third-party applications for specialised business operations. This approach allows the core platform to remain clean, lightweight, and easy for everyday business owners to navigate.

As you can see based on my conservative assumption Intuit is looking to grow 10% over the long run so I went conservative and assumed a 8% growth in the first 1-3 years then the growth will slow down to 5% 4-6 years out. In my assumption I also went with an exit multiple of 15x earnings which is below the historical average at which Intuit has traded. Based on my assumption I have come to a buy price of $370.45 compared to the current stock price of $261.00 which means right now Inuit is trading below its intrinsic value.

Thanks for reading my newsletter on Intuit.

Disclaimer: This newsletter is not financial advice. This is for educational purposes only, so please DO NOT take this as a buy or sell signal.

Follow for more:

Remember to subscribe, share, and comment below if you find this newsletter insightful. Your support helps me continue my work.